Ever wanted help with a project? What if you could exchange needed services with your friends and neighbors? This group did just that through the time-banking model.

Ever wanted help with a project? What if you could exchange needed services with your friends and neighbors? This group did just that through the time-banking model.

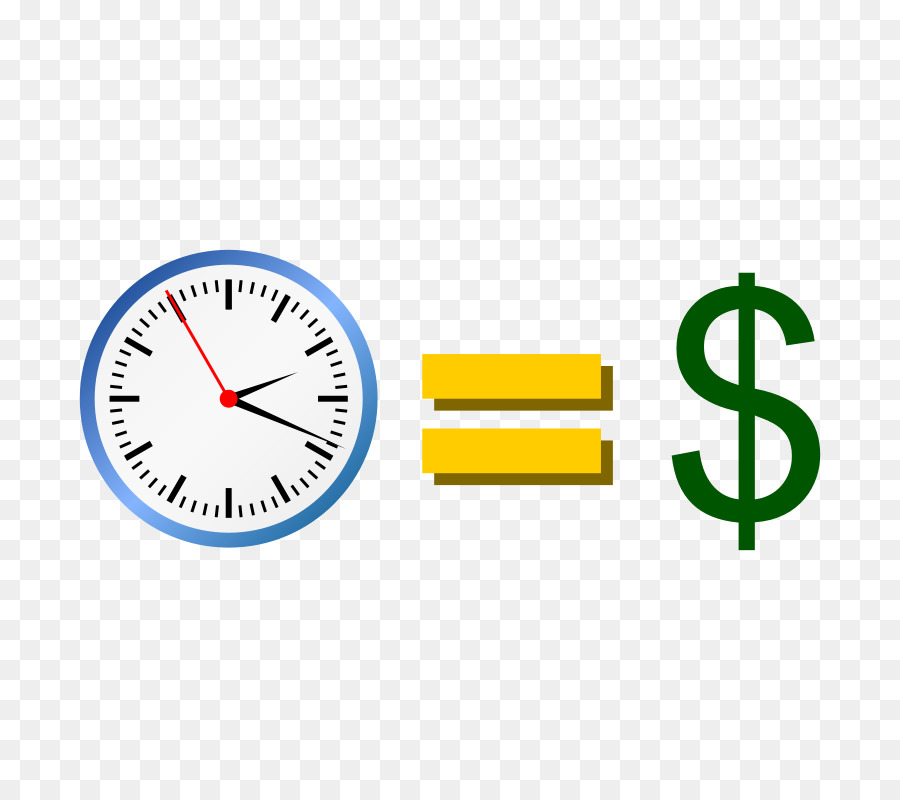

Time-banking is a model for trading skills, goods, and labor instead of money—a sort of barter system where members “deposit” hours doing things like teaching, cooking, or repairing things, and “withdraw” hours of other members’ services. It’s been around in the U.S. since the 1980s, and there are close to 500 such banks across the country today. No Price Tags: These Neighbors Built Their Own Economy Without Money

Most function on a one-hour to one-hour system that helps members meet their needs in non-monetary ways, often saving money. This allows stay-at-home mothers, retirees, and business professionals alike to contribute.